One More Reason to Refinance4/27/2020  Taking cash out of the equity of your home could be a legitimate way to fund a temporary cash crisis now or to have it on-hand if the need arises. Most homeowners can pull out the difference in 80% of the fair market value of their home and what they currently owe.

The most frequently cited reasons for refinancing are to lower the payment, eliminate the private mortgage insurance, combine mortgages, consolidate debt, convert an ARM to a fixed rate mortgage, remove a person from the loan or to take cash out for another reason. The option of using your equity to deal with unexpected living expenses or potential lost wages in the future could be a good reason for doing a cash-out refinance. It is important to consider that it could increase your monthly payment instead of lowering it which would result in higher expenses during uncertain economic times. Some lenders have recently raised the minimum credit score requirement but borrowers with good credit and the ability to repay should be able to refinance. Lenders are reporting that during the Covid-19 crisis their processing time is taking longer but they have implemented procedures to safely facilitate the application as well as the appraisals. While homeowners with an FHA loan are available for a streamline process because FHA is already insuring the mortgage to be refinanced, the cash-out is limited to $500. Even though the owner may not be able to pull funds out of their FHA equity, refinancing may lower their payment and therefore, lower their expenses. Unlike conventional loans that require income through a job or other sources, refinancing an existing FHA loan does not require income verification or an appraisal. The borrower cannot be delinquent on their current FHA loan and it must be at least six months old. The refinance must reduce the current interest rate or term or both. Another alternative for homeowners is a HELOC, home equity line of credit, where you do not incur interest expense unless you actually draw on the line of credit. It will be a variable rate home equity loan similar to a credit card letting you borrow up to a specific limit when you want and repay it slowly over time. Refinancing a home incurs closing costs which can be paid in cash or added to the financed amount. The breakeven point to recapture the cost of refinancing is determined by dividing the monthly savings into the cost of refinancing. If you stay in the home less than that time, refinancing could be an unnecessary expense.

0 Comments

Reverse Mortgage1/13/2020  Reverse mortgage loans are like traditional mortgages that permits homeowners to borrow money using their home as collateral while retaining title to the property. Reverse mortgage loans don't require monthly payments.

The loan is due and payable when the borrower no longer lives in the home or dies, whichever comes first. Since no payments are made, interest and fees earned are added to the loan balance each month causing an increasing unpaid balance. Homeowners are required to pay property taxes, insurance and maintain the home, as their principal residence, in good condition. Reverse mortgages provide older Americans including Baby Boomers access to their home's equity. Borrowers can use their equity to renovate their homes, eliminate personal debt, pay medical expenses or supplement their income with reverse mortgage funds. Homeowners are required to be 62 years and older and meet the following requirements:

Payouts are based on the age of the youngest spouse. The younger the age, the less money can be borrowed. Reverse mortgages offer two terms ... a fixed rate or variable rate. Fixed rate HECMs have one interest rate and one lump sum payment. Variable rate loans offer multiple payout options:

Traditional reverse mortgages, also called Home Equity Conversion Mortgage, HECM, are insured by FHA. There are no income limitations or requirements and the loan funds may be used for any purpose. The borrower must attend a counseling session about the HECM, its risk, benefits, and how much can be borrowed. The final loan amount is based on borrower's age and home value. FHA HECMs require upfront and annual mortgage insurance premiums but can be wrapped into the loan. Proprietary HECM loans are not federally insured. Lenders create their own terms, including allowing loan amounts higher than the FHA maximum. Proprietary HECMs don't require mortgage insurance (upfront or monthly), which may result in more funds available. Proprietary reverse mortgages typically have higher interest rates than FHA HECMs. Advantages

Disadvantages

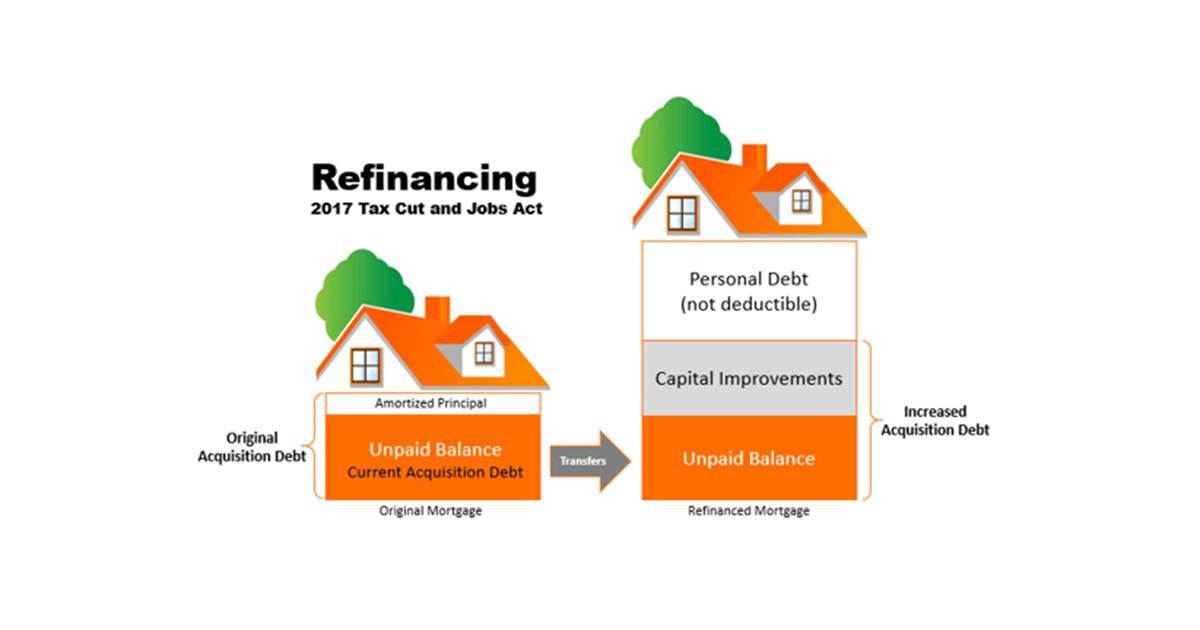

More information is available about reverse mortgages from the Consumer Financial Protection Bureau or Federal Trade Commission or HUD.gov. Questions? Prefer to discuss further? Give Jenni a call at (808) 345-6192  Mortgage interest paid on your principal residence is deductible today as it was in 1913 when 16th amendment allowed personal income tax. The 2017 Tax Cut and Jobs Act reduced the maximum amount of acquisition debt from $1,000,000 to $750,000.

Acquisition debt is the amount of debt used to buy, build or improve a principal residence, up to the maximum amount. A common misunderstanding among taxpayers is that you are entitled to that much debt even if you refinance a home during your ownership years. Acquisition debt is a dynamic number that changes over time. It decreases with normal amortization as the principal amount of debt is reduced. The only way to increase acquisition debt after a home is purchased is to borrow additional funds that are used for capital improvements. Assume a person buys a home with a new mortgage and after the home has enjoyed significant appreciation, refinances the home for much more than is currently owed. Let's also say that the refinance amount is less than $750,000 which might lead the borrower to an erroneous conclusion that all the interest will be deductible. The current acquisition debt is transferred to the new mortgage. Only the portion of the funds used to pay for new capital improvements can be combined to equal the increased acquisition debt. The interest on that part of the mortgage is deductible as qualified mortgage interest. The remainder of the refinanced mortgage is attributed to personal debt and the interest paid on that is not deductible. Lenders are not generally concerned with making a homeowner a fully tax-deductible loan. Lenders are interested in making a loan which will make a profit and be repaid according to the terms. The annual statements that most lenders issue to borrowers indicate how much interest was paid in a calendar year as they are required to do by federal law. Part of the confusion may be because homeowners believe they can deduct interest on debt up to $750,000 and this annual statement shows the interest paid for the year. It is up to each homeowner to keep track of their acquisition debt and only deduct the qualified mortgage interest. Your tax professional can be very helpful in determining this amount. It is important to notify them that you have refinanced a home during the tax year for which the taxes are being reported. For more information, see IRS Publication 936 and Homeowners Tax Guide. Home equity debt has not been allowed since the beginning of 2018. AuthorRead helpful articles and real estate resources shared on behalf Realtor® Broker, BIC Jennifer R. Rhodes of Premier Island Properties LLC Archives

June 2020

Categories

All

|

RSS Feed

RSS Feed

|

RB-22237

|

|