Shopping for a Mortgage3/9/2020  A lower rate will not only result in a lower payment, it will amortize the loan quicker. A $250,000 mortgage at 4.5% for 30 years will have a $1,266.71 principal and interest payment. At 4%, the same loan will have $1,193.54 payment saving $73.18 a month and the unpaid balance would be $1,776 lower at the end of five years.

Mortgage lenders tend to price their mortgages based on the credit score of the borrower. The higher the credit score, the lower the mortgage rate. There is an inverse relationship that the lower the credit score, the higher risk and therefore, a higher rate is needed to balance the risk. In order to get a valid rate that will be available to you with your credit score, you need to be pre-approved. The process of making a loan application before you find a home, allows the lender to verify your credit, income, and ability to repay the loan. Lenders usually only charge the cost of the credit report for this type of service. Be aware that pre-approval is not the same thing as pre-qualification which is simply a loan officer's opinion. When you shop for a mortgage with multiple lenders, the credit bureaus count them as a single credit inquiry if they are done within a two-week period. On the other hand, restrain yourself from applying for other credit such as cars, furniture or credit cards until after you have closed on the purchase of your home because those inquiries can negatively affect your credit score. The Consumer Financial Protection Bureau recommends that you let lenders know that you are shopping the mortgage for the best rate and fees. Instead of going to the Internet and Googling mortgage lenders, start with recommendations for a lender from your real estate professional. They see the good, the bad and the ugly and can save you a lot of time. Another reliable source would be from a friend who has recently purchased a home. There are lenders who bait unsuspecting borrowers with lower rates and fees into making an application and after critical time has lapsed, try to switch them to a different program. By that point, many buyers feel they don't have any choice but to accept what is offered. Another confusing factor is the way that loans are priced to the public. They are usually quoted at a rate with a certain amount of points. A point is one percent of the amount borrowed. An example would be a quote for a loan at 4.5% with 1 point or at 4% with 2.5 points. The points combined with the rate affect the yield the lender will earn, and you will pay. A simple way to make this an apple to apple comparison is to have the lender quote the loan as a "par-value" loan with no points involved. Then, the lowest rate will produce the lowest cost to you. Another way to compare loans will be to uses a financial app called Will Points Make a Difference. You can plug in the rate and points to calculate the lowest yield over a projected holding period or the full term. The lenders do not want to make it easy for you to compare. Mortgage money is a commodity and shopping will be worth the effort. Ready to start shopping?

0 Comments

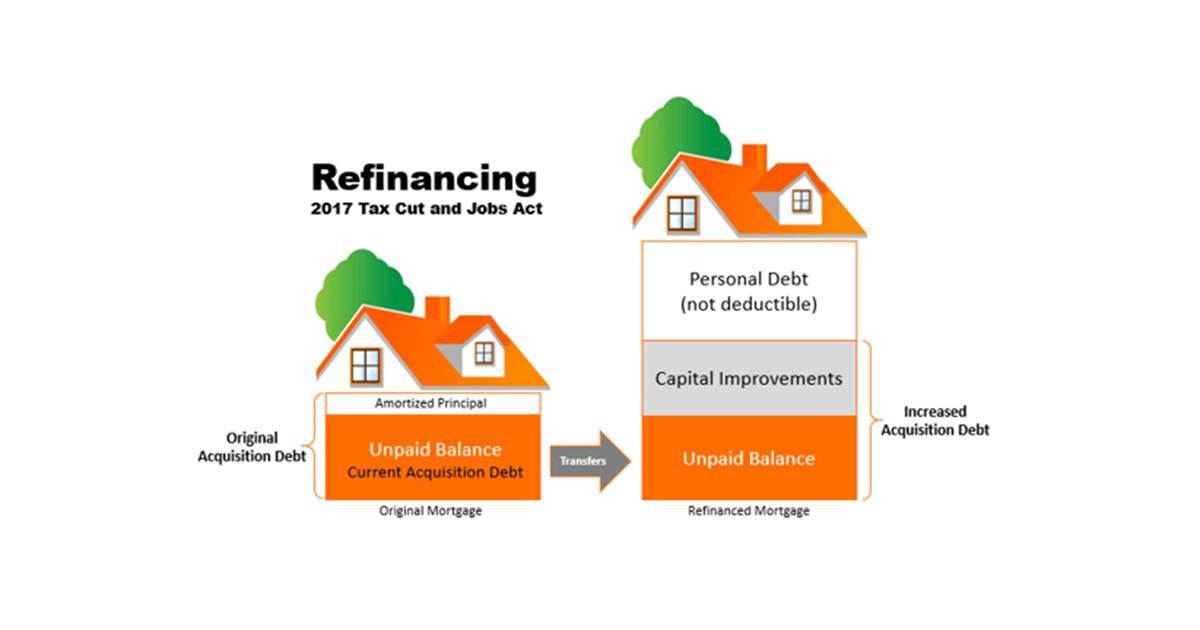

Mortgage interest paid on your principal residence is deductible today as it was in 1913 when 16th amendment allowed personal income tax. The 2017 Tax Cut and Jobs Act reduced the maximum amount of acquisition debt from $1,000,000 to $750,000.

Acquisition debt is the amount of debt used to buy, build or improve a principal residence, up to the maximum amount. A common misunderstanding among taxpayers is that you are entitled to that much debt even if you refinance a home during your ownership years. Acquisition debt is a dynamic number that changes over time. It decreases with normal amortization as the principal amount of debt is reduced. The only way to increase acquisition debt after a home is purchased is to borrow additional funds that are used for capital improvements. Assume a person buys a home with a new mortgage and after the home has enjoyed significant appreciation, refinances the home for much more than is currently owed. Let's also say that the refinance amount is less than $750,000 which might lead the borrower to an erroneous conclusion that all the interest will be deductible. The current acquisition debt is transferred to the new mortgage. Only the portion of the funds used to pay for new capital improvements can be combined to equal the increased acquisition debt. The interest on that part of the mortgage is deductible as qualified mortgage interest. The remainder of the refinanced mortgage is attributed to personal debt and the interest paid on that is not deductible. Lenders are not generally concerned with making a homeowner a fully tax-deductible loan. Lenders are interested in making a loan which will make a profit and be repaid according to the terms. The annual statements that most lenders issue to borrowers indicate how much interest was paid in a calendar year as they are required to do by federal law. Part of the confusion may be because homeowners believe they can deduct interest on debt up to $750,000 and this annual statement shows the interest paid for the year. It is up to each homeowner to keep track of their acquisition debt and only deduct the qualified mortgage interest. Your tax professional can be very helpful in determining this amount. It is important to notify them that you have refinanced a home during the tax year for which the taxes are being reported. For more information, see IRS Publication 936 and Homeowners Tax Guide. Home equity debt has not been allowed since the beginning of 2018. AuthorRead helpful articles and real estate resources shared on behalf Realtor® Broker, BIC Jennifer R. Rhodes of Premier Island Properties LLC Archives

June 2020

Categories

All

|

RSS Feed

RSS Feed

|

RB-22237

|

|