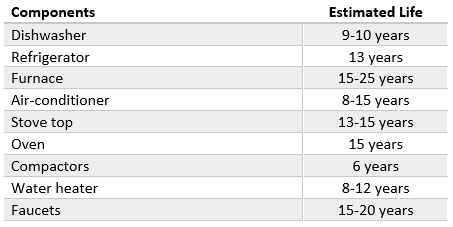

Anticipating the Cost of a Home12/23/2019  The largest expenditure a buyer has when purchasing a home is the down payment which can range from zero for veterans or 3.5%, 5%, 10% and 20%. With mortgages come closing costs which can be another 2-4% and must be paid at settlement in cash. Most mortgages require an escrow account to pay the property taxes and insurance when they are due. Generally, the lender will require one to three months of taxes and one month of insurance so they can be paid before the actual due date. First-time buyers should be aware that they'll need this amount of funds available to purchase a home. Unlike tenants who are not responsible for repairs, homeowners are, and it is necessary to be able to pay for them when they're needed. Newer homes will need less repairs and older homes probably, more. At some point, components like the furnace, air-conditioner and appliances will need to be replaced which could crush a homeowner's budget if they are not expecting them. Homeowners should expect between one and four percent of the value of the home in annual repairs. The age and condition of the home and whether some of the items have been replaced will help assess the anticipated expenditures.  A $175,000 home with 2% estimated repair expenditures would be $3,500 a year or about $300 per month. Some years, it may not run that much and other years, it might be more. By anticipating the maintenance expenses, a homeowner is more likely to handle things when they arise.

Another way to handle the risk of unexpected repair expenses would be to purchase a home warranty. For $500 -700 a year, repairs and sometimes, replacements will be handled by the protection plan. Call me at (808) 345-6192 for a list of trusted protection plans available in our area.

0 Comments

Personal Finance Review12/16/2019  Even if Benjamin Franklin never actually used the expression "a penny saved is a penny earned", the reality is that it has been a sentiment for frugality for centuries. He did say: "Beware of little expenses; a small leak will sink a great ship." At the end of the day, it is not about how much you make as much as it is about how much you keep.

The first step in a personal finance review is to discover where you are spending your money. It can be very eye-opening to have a detailed accounting of all the money you spend. Coffee breaks, lunches, entertainment, happy hour, groceries and the myriad of subscription services you have contribute to your spending. This revelation can lead you to obvious areas where savings can be accomplished. The next step is to dig a little deeper to see if there are possible savings on essential services.

A strategy that some people use is to report their credit cards as lost so new cards will be issued. When they are contacted by the companies to get a valid credit card, they can determine if the service is still needed. The money you save can ultimately help you in the future for a rainy day, an unanticipated expense, a major life event or retirement. Cutting back now will give you more later, possibly, when you need it even more. Tennessee Williams said "You can be young without money, but you can't be old without it." An Investment Perspective on a Home12/10/2019  Looking for an investment that will turn $10,000 into $80,000 in seven years? Sound too good to be true? What if I told you that you could live in it every day during that seven years? Would that sound even better?

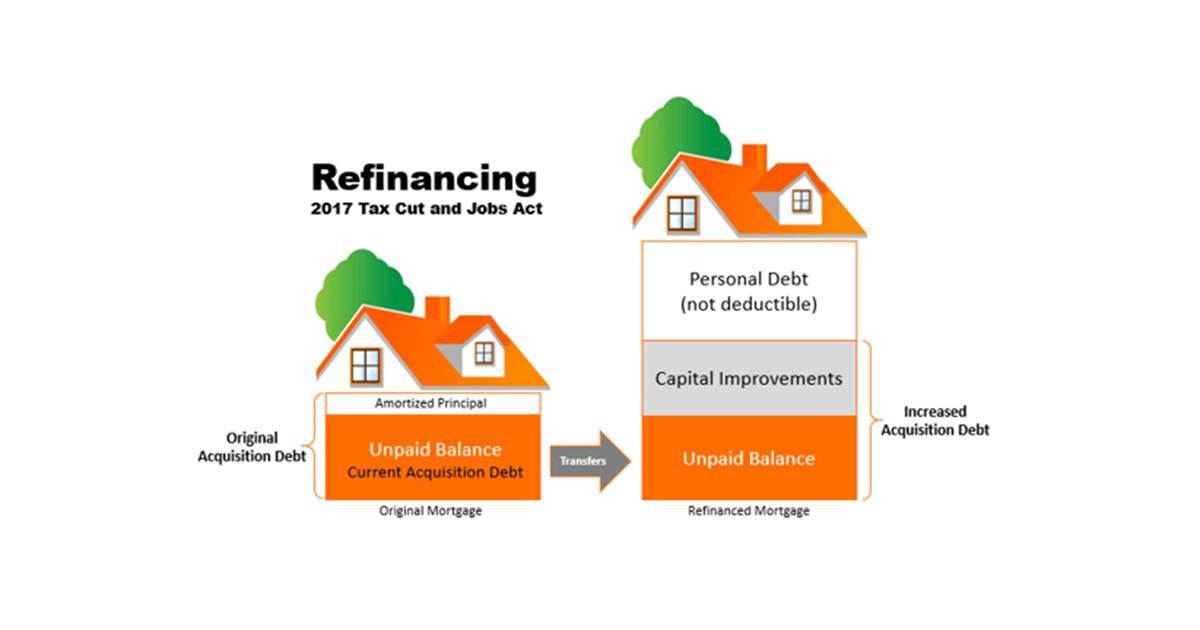

A $300,000 home purchased today on an FHA loan would have a $10,500 down payment. If it appreciated at 2% annually, which is less than the U.S. average, the future value of the home would be $344,606 in seven years. The unpaid balance on the loan would be $256,350 based on normal amortization which would make the equity in the home $88,256. The annual compound rate of return on the down payment would be 35%. This number sounds so large, that you might start doubting the credibility of this example. Looking at some alternative investments, a ten-year Treasury note is currently paying 1.73%. You can earn 2.1% on a ten-year certificate of deposit. If you could handle the volatility of the stock market and pick the right stock, you might earn 7-10%. There really is no alternative investment that can earn the return that an owner-occupied home can offer while giving you the ability to live and enjoy the home during the holding period. Even if you could find an investment that paid a good return, when you realize the gain, you'll be required to pay income tax, either at long-term capital gains rates or ordinary income. However, a person who has lived in a home for at least two of the last five years can exclude up to $250,000 of gain from their income if they are single and up to $500,000 of gain if the owners are married, filing jointly. A home can certainly be a place of your own to feel safe and secure, to raise your family, share with friends and build memories. A home could be considered an emotional investment and one that pays big dividends. A home is also a financial investment not just for the reasons mentioned above but also because the equity can be accessed by doing a cash-out refinance or a home equity line of credit. See what your investment might look like by using the Rent vs. Own and giving us a call at .  Mortgage interest paid on your principal residence is deductible today as it was in 1913 when 16th amendment allowed personal income tax. The 2017 Tax Cut and Jobs Act reduced the maximum amount of acquisition debt from $1,000,000 to $750,000.

Acquisition debt is the amount of debt used to buy, build or improve a principal residence, up to the maximum amount. A common misunderstanding among taxpayers is that you are entitled to that much debt even if you refinance a home during your ownership years. Acquisition debt is a dynamic number that changes over time. It decreases with normal amortization as the principal amount of debt is reduced. The only way to increase acquisition debt after a home is purchased is to borrow additional funds that are used for capital improvements. Assume a person buys a home with a new mortgage and after the home has enjoyed significant appreciation, refinances the home for much more than is currently owed. Let's also say that the refinance amount is less than $750,000 which might lead the borrower to an erroneous conclusion that all the interest will be deductible. The current acquisition debt is transferred to the new mortgage. Only the portion of the funds used to pay for new capital improvements can be combined to equal the increased acquisition debt. The interest on that part of the mortgage is deductible as qualified mortgage interest. The remainder of the refinanced mortgage is attributed to personal debt and the interest paid on that is not deductible. Lenders are not generally concerned with making a homeowner a fully tax-deductible loan. Lenders are interested in making a loan which will make a profit and be repaid according to the terms. The annual statements that most lenders issue to borrowers indicate how much interest was paid in a calendar year as they are required to do by federal law. Part of the confusion may be because homeowners believe they can deduct interest on debt up to $750,000 and this annual statement shows the interest paid for the year. It is up to each homeowner to keep track of their acquisition debt and only deduct the qualified mortgage interest. Your tax professional can be very helpful in determining this amount. It is important to notify them that you have refinanced a home during the tax year for which the taxes are being reported. For more information, see IRS Publication 936 and Homeowners Tax Guide. Home equity debt has not been allowed since the beginning of 2018. AuthorRead helpful articles and real estate resources shared on behalf Realtor® Broker, BIC Jennifer R. Rhodes of Premier Island Properties LLC Archives

June 2020

Categories

All

|

RSS Feed

RSS Feed

|

RB-22237

|

|