Downsizing in 20201/6/2020  Approximately 52 million or 16% of Americans are age 65 and over. It is easy to understand that some of them are thinking of downsizing their home because they don't need the same space they did in the past.

It can be liberating to divest yourself of "things" that have been accumulated over the years but are no longer needed. Moving to a less expensive home, could provide savings for unanticipated expenditures or cash that could be invested for additional income. Savings can be realized in the lower premiums for insurance and lower property taxes, as well as, the lower utility costs associated with a smaller home. Typically, owners downsize to a home to 2/3 to 50% of their current home's size. In some situations, it is not only economically beneficial, but their interests may have changed so that a different style of home, area or city might fit their lifestyle better. The sale of a home with a lot of profit will not necessarily trigger a tax liability. Homeowners are eligible for an exclusion of $250,000 of gain for single taxpayers and up to $500,000 for married taxpayers who have owned and used their home two out of the last five years and haven't taken the exclusion in the previous 24 months. Homeowners should consult their tax professionals to see how this may apply to their individual situation. For more information, you can download the Homeowners Tax Guide. Call me at (808) 345-6192 to find out what your home is worth and what it would take to make the move to another home.

0 Comments

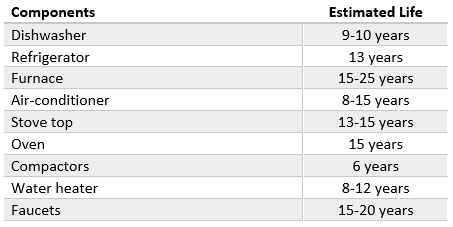

Anticipating the Cost of a Home12/23/2019  The largest expenditure a buyer has when purchasing a home is the down payment which can range from zero for veterans or 3.5%, 5%, 10% and 20%. With mortgages come closing costs which can be another 2-4% and must be paid at settlement in cash. Most mortgages require an escrow account to pay the property taxes and insurance when they are due. Generally, the lender will require one to three months of taxes and one month of insurance so they can be paid before the actual due date. First-time buyers should be aware that they'll need this amount of funds available to purchase a home. Unlike tenants who are not responsible for repairs, homeowners are, and it is necessary to be able to pay for them when they're needed. Newer homes will need less repairs and older homes probably, more. At some point, components like the furnace, air-conditioner and appliances will need to be replaced which could crush a homeowner's budget if they are not expecting them. Homeowners should expect between one and four percent of the value of the home in annual repairs. The age and condition of the home and whether some of the items have been replaced will help assess the anticipated expenditures.  A $175,000 home with 2% estimated repair expenditures would be $3,500 a year or about $300 per month. Some years, it may not run that much and other years, it might be more. By anticipating the maintenance expenses, a homeowner is more likely to handle things when they arise.

Another way to handle the risk of unexpected repair expenses would be to purchase a home warranty. For $500 -700 a year, repairs and sometimes, replacements will be handled by the protection plan. Call me at (808) 345-6192 for a list of trusted protection plans available in our area. Personal Finance Review12/16/2019  Even if Benjamin Franklin never actually used the expression "a penny saved is a penny earned", the reality is that it has been a sentiment for frugality for centuries. He did say: "Beware of little expenses; a small leak will sink a great ship." At the end of the day, it is not about how much you make as much as it is about how much you keep.

The first step in a personal finance review is to discover where you are spending your money. It can be very eye-opening to have a detailed accounting of all the money you spend. Coffee breaks, lunches, entertainment, happy hour, groceries and the myriad of subscription services you have contribute to your spending. This revelation can lead you to obvious areas where savings can be accomplished. The next step is to dig a little deeper to see if there are possible savings on essential services.

A strategy that some people use is to report their credit cards as lost so new cards will be issued. When they are contacted by the companies to get a valid credit card, they can determine if the service is still needed. The money you save can ultimately help you in the future for a rainy day, an unanticipated expense, a major life event or retirement. Cutting back now will give you more later, possibly, when you need it even more. Tennessee Williams said "You can be young without money, but you can't be old without it." An Investment Perspective on a Home12/10/2019  Looking for an investment that will turn $10,000 into $80,000 in seven years? Sound too good to be true? What if I told you that you could live in it every day during that seven years? Would that sound even better?

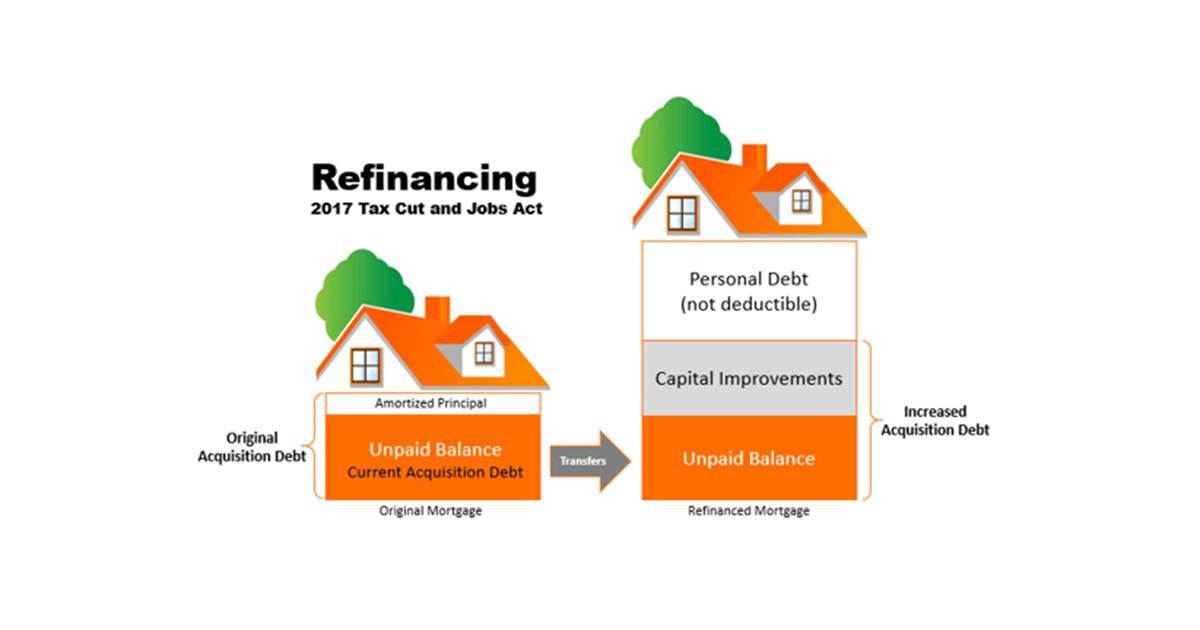

A $300,000 home purchased today on an FHA loan would have a $10,500 down payment. If it appreciated at 2% annually, which is less than the U.S. average, the future value of the home would be $344,606 in seven years. The unpaid balance on the loan would be $256,350 based on normal amortization which would make the equity in the home $88,256. The annual compound rate of return on the down payment would be 35%. This number sounds so large, that you might start doubting the credibility of this example. Looking at some alternative investments, a ten-year Treasury note is currently paying 1.73%. You can earn 2.1% on a ten-year certificate of deposit. If you could handle the volatility of the stock market and pick the right stock, you might earn 7-10%. There really is no alternative investment that can earn the return that an owner-occupied home can offer while giving you the ability to live and enjoy the home during the holding period. Even if you could find an investment that paid a good return, when you realize the gain, you'll be required to pay income tax, either at long-term capital gains rates or ordinary income. However, a person who has lived in a home for at least two of the last five years can exclude up to $250,000 of gain from their income if they are single and up to $500,000 of gain if the owners are married, filing jointly. A home can certainly be a place of your own to feel safe and secure, to raise your family, share with friends and build memories. A home could be considered an emotional investment and one that pays big dividends. A home is also a financial investment not just for the reasons mentioned above but also because the equity can be accessed by doing a cash-out refinance or a home equity line of credit. See what your investment might look like by using the Rent vs. Own and giving us a call at .  Mortgage interest paid on your principal residence is deductible today as it was in 1913 when 16th amendment allowed personal income tax. The 2017 Tax Cut and Jobs Act reduced the maximum amount of acquisition debt from $1,000,000 to $750,000.

Acquisition debt is the amount of debt used to buy, build or improve a principal residence, up to the maximum amount. A common misunderstanding among taxpayers is that you are entitled to that much debt even if you refinance a home during your ownership years. Acquisition debt is a dynamic number that changes over time. It decreases with normal amortization as the principal amount of debt is reduced. The only way to increase acquisition debt after a home is purchased is to borrow additional funds that are used for capital improvements. Assume a person buys a home with a new mortgage and after the home has enjoyed significant appreciation, refinances the home for much more than is currently owed. Let's also say that the refinance amount is less than $750,000 which might lead the borrower to an erroneous conclusion that all the interest will be deductible. The current acquisition debt is transferred to the new mortgage. Only the portion of the funds used to pay for new capital improvements can be combined to equal the increased acquisition debt. The interest on that part of the mortgage is deductible as qualified mortgage interest. The remainder of the refinanced mortgage is attributed to personal debt and the interest paid on that is not deductible. Lenders are not generally concerned with making a homeowner a fully tax-deductible loan. Lenders are interested in making a loan which will make a profit and be repaid according to the terms. The annual statements that most lenders issue to borrowers indicate how much interest was paid in a calendar year as they are required to do by federal law. Part of the confusion may be because homeowners believe they can deduct interest on debt up to $750,000 and this annual statement shows the interest paid for the year. It is up to each homeowner to keep track of their acquisition debt and only deduct the qualified mortgage interest. Your tax professional can be very helpful in determining this amount. It is important to notify them that you have refinanced a home during the tax year for which the taxes are being reported. For more information, see IRS Publication 936 and Homeowners Tax Guide. Home equity debt has not been allowed since the beginning of 2018. Title Insurance11/25/2019  Most people who have car, home and health insurance have probably made claims and wouldn't consider being without it. However, it might be difficult to find a homeowner who has made a claim on their title insurance which could lead a person to think that it may not be necessary.

Title insurance covers the largest investment most people have and if there was a loss, it could be devastating. Title insurance indemnifies the policy holder from financial loss sustained from defects in the title to the property. The policy holder is determined by their interest in the property. An owner's title policy protects the owner of the property from title issues that may arise other than the mortgages that are being placed on the property at the time of purchase. The title of the property goes back in time to check that clear title (no unsatisfied liens or levies and poses no question to legal ownership) was passed from owner to owner up to the current seller. A mortgagee's or lender's policy protects the lender by guaranteeing they have an enforceable lien on the property and legal claims from parties asserting they have a claim against the property. Lender's generally require the borrower to provide this coverage. The title search is an examination to determine and confirm legal ownership and if there are clouds on the title so the seller can pass a clear title. A cloud is defined as any document, claim, unreleased lien or encumbrance that might invalidate or impair the title to real property. If a person passes title to a buyer that has unsatisfied liens on the property, the new buyer could become responsible for the money owed and it could affect their ability to sell the property in the future. Unlike most insurance that has a specific term and periodic premiums, title insurance covers the insured for a single premium. An owner's policy lasts for as long as they or their heirs have an interest in the property. It guarantees the title up to the date and time that the property was deeded to you and recorded in the public records. The majority of homes purchased in America have title policies insuring the new owner. You could live in the home for five, ten or twenty years without an incident. Then, when you're ready to sell the home, a title claim could happen. The title policy would still protect you at that point. It is a peace of mind coverage that is part of the investment in your home. 7 Reasons to Buy a Home11/18/2019  Some people don't need a reason to buy a home, they just want it. That can be enough justification by itself. Other people need some solid logic before they're ready to make the commitment. The following reasons might help you to make a decision.

A bonus reason to buy a home now are the low mortgage rates available. The lowest rate recorded by Freddie Mac is 3.35% in December 2012. Today's rates are 3.75% on a 30-year fixed rate mortgage and 3.21% on a 15-year fixed rate mortgage. So, they are certainly very close to all-time lows. The highest rate on a 30-year fixed rate mortgage was 18.45% in October 1981. When you put today's rates in perspective, they are an incredible bargain. Many industry experts expect that they will not remain as low as they are now. Locking in a low rate can keep your housing costs low. A $275,000 mortgage at 3.75% for 30 years has a principal and interest payment of $1,273.57. If the rate goes up by 1%, the payment would increase to $1,434.53 or $160.96 per month for the 30-year term. Check the Rent vs. Own to see how the numbers look in your situation.  Before looking for a home, you need to know how much you can afford. While you may have a number in your head, the lender has the final say. Securing a pre-approval from a lender helps make the home buying process easier and helps to avoid delays.

Many buyers confuse the terms pre-qualification and pre-approval. They mean two different things. In simple terms, a pre-qualification is an estimate of what you can afford. A pre-approval is a conditional approval based on the proof you provide. The pre-qualification is a preliminary step some borrowers take to get a feel for what price home they can afford. Based on your income, assets, and estimated credit score, lenders can estimate what you can afford. It's important to know, there's nothing binding about a pre-qualification. It's simply a starting point. When you are serious about buying a home, though, you want a pre-approval. Before you shop for a home, meet with a recommended lender to get a pre-approval letter. Sellers and/or Realtors value this letter because it shows you are likely to secure the necessary financing and serious about buying a home. Lenders meet with you in person to create the pre-approval. You'll provide the lender with all the following:

Lenders evaluate the documents and determine your conditional approval. The letter will state the mortgage amount you qualify for, the loan's terms, and any conditions the approval is contingent upon. Normally, final approval is contingent on a fully executed sales contract of the property to be purchased, a satisfactory appraisal and clear title on the property. Once a purchase contract is signed, the lender completes the underwriting on your loan. They will confirm that the property meets the necessary requirements. The lender will also re-confirm your income, assets, employment, and credit information before closing on the loan. Securing a pre-approval prior to beginning the home buying process will give you confidence and can help your negotiations with the seller. Your REALTOR® can provide you more information in an Buyers Guide and recommendations of trusted lenders. Buy Your Retirement Home Now11/4/2019  Maybe you're not ready to move into it but that doesn't mean that you shouldn't take advantage of the present opportunities to acquire the home you want to live in during retirement. The combination of the low mortgage rates, high rental rates, positive cash flows and tax advantages can help you get it paid for by the time you're ready to move into it.

Your tenant could literally buy your retirement home for you. One idea would be to finance it with a 15-year loan that will have a lower rate than a 30-year loan and it will obviously be paid for in half the time. With every monthly rental check from your tenant, you make the payment on the mortgage which includes a portion that reduces debt and builds equity. Even if you don't have the home paid for by the time you retire, your equity will be larger. Consider you sell your current home which could be paid for by then when you are ready to move into this retirement home. Taxpayers can exclude up to $500,000 of tax-free gain for a married couple. That profit could be used to fund your retirement. Even if you don't retire to this home, it could be a placeholder to control the costs of the home you do move into. For example, you could buy a home in a destination location now, rent it out and build equity in it until you're ready to use it as your principal residence. That home would have kept pace with other homes in the area so that you would not be priced out of the market you want to retire to. With home prices and mortgage rates certain to rise, this may be one of the best decisions you can make. We want to be your personal source of real estate information and we're committed to helping from purchase to sale and all the years in between. Contact us if you'd like to talk about the idea or if you need a recommendation of real estate professional in another city. A Good Time to Buy a Home10/28/2019 You may have noticed that REALTORS® seem to always think now is a good time to buy and they can usually justify it with solid reasoning. While it can be true in general, a good time to buy has more to do with the individual than anything else. There are four things to consider. It is a good time to buy a home when you have good credit. Since the Great Recession and the housing crisis, lenders have been required to be sure that the borrowers have good credit. This actually benefits not only the lenders but the borrowers because no one wants to buy something that they cannot afford and run the risk of losing it to foreclosure. FHA has the most lenient FICO credit score of 580+. VA requires a little higher at 620 while Fannie Mae guidelines on conventional mortgages require a 700 score. It is a good time to buy a home when you have a good job that gives you the income to qualify for the mortgage and the likelihood that you'll continue to be employed in the future. Two years of steady employment in the same industry with no significant gaps is a measure that lenders consider. Lenders use qualifying ratios to make a determination. The total house payment, principal, interest, taxes and insurance, should not exceed 28% of the borrower's monthly gross income. Their total monthly debt including the house payment should not exceed 45% of monthly gross income. There is some flexibility in the ratios for the right circumstances. It is a good time to buy a home when you have the available funds for the down payment and closing costs plus a little cushion for the unexpected. The down payments can range from 0% for VA loans to 3.5% for FHA and 3% to 20% for conventional. In addition to the down payment, borrowers will have closing costs that can range from 2 to 3.5% depending on the loan type. It is possible for the seller to pay the buyer's closing costs but it needs to be negotiated in the sales contract. The lender's underwriter wants borrowers to have cash available for unexpected expenses related to the house and their normal living expenses. It is a good time to buy a home when you have stability ... In addition to employment, stability applies to not moving soon, marital status, children and unanticipated expenses. Market or economic conditions could also affect stability. So, the answer to the question "is it a good time to buy a home" depends on several things that are relative to the buyer. While it might be a great time to buy for one buyer, it may not be the best time for another buyer. Make a self-assessment to the best of your knowledge on these issues and then, schedule an appointment for a live interview with a trusted mortgage professional to get their opinion based on what underwriting will look at. Call me at (808) 345-6192 if you'd like a recommendation. After you determine it is a good time to buy a home, it is time to meet with your real estate professional. Ready to buy a home?

AuthorRead helpful articles and real estate resources shared on behalf Realtor® Broker, BIC Jennifer R. Rhodes of Premier Island Properties LLC Archives

June 2020

Categories

All

|

RSS Feed

RSS Feed

|

RB-22237

|

|